Latest

Distribution and Integration Versus Capital and...

AI investment remains intense even as short-term profitability is unclear. H100 rental prices continue to decline and medium-sized clusters are easier to obtain, yet demand persists across a widening buyer...

Distribution and Integration Versus Capital and...

AI investment remains intense even as short-term profitability is unclear. H100 rental prices continue to decline and medium-sized clusters are easier to obtain, yet demand persists across a widening buyer...

Directed Self-Assembly for Intel 14A High-NA EU...

Intel’s 18A node has dominated headlines, but 14A is the pivotal generation for winning large, high-value foundry customers. Early 18A engagements will likely target lower-risk designs; if those succeed, 14A...

Directed Self-Assembly for Intel 14A High-NA EU...

Intel’s 18A node has dominated headlines, but 14A is the pivotal generation for winning large, high-value foundry customers. Early 18A engagements will likely target lower-risk designs; if those succeed, 14A...

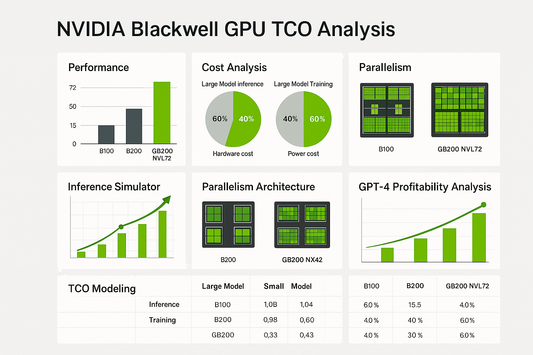

Performance and Cost Modeling for Large and Sma...

NVIDIA’s B100, B200, and GB200 announcements sparked questions beyond headline TFLOPS: how do they change performance per total cost of ownership (TCO) for training and inference, and what does that...

Performance and Cost Modeling for Large and Sma...

NVIDIA’s B100, B200, and GB200 announcements sparked questions beyond headline TFLOPS: how do they change performance per total cost of ownership (TCO) for training and inference, and what does that...

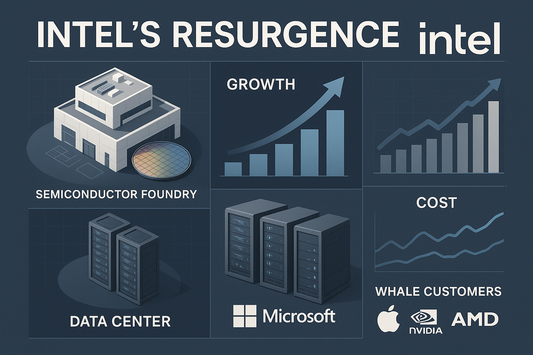

Whale Customers and Capacity Commitments in Int...

Intel spent the 2010s eroding its strategic position through financial engineering and missed platform shifts, notably declining the iPhone modem/SoC opportunity over margin concerns. Lost mobile volume fed competitors’ learning...

Whale Customers and Capacity Commitments in Int...

Intel spent the 2010s eroding its strategic position through financial engineering and missed platform shifts, notably declining the iPhone modem/SoC opportunity over margin concerns. Lost mobile volume fed competitors’ learning...

Optical DSP Growth in 800 Gb/s and 1.6 Tb/s Ramps

NVIDIA’s Blackwell portfolio spans multiple SKUs and form factors, but the flagship is the vertically integrated DGX GB200 NVL72: a single rack with 72 GPUs, 36 CPUs, 18 NVSwitches, 72...

Optical DSP Growth in 800 Gb/s and 1.6 Tb/s Ramps

NVIDIA’s Blackwell portfolio spans multiple SKUs and form factors, but the flagship is the vertically integrated DGX GB200 NVL72: a single rack with 72 GPUs, 36 CPUs, 18 NVSwitches, 72...

Ramp Outlook: B100, B200, GB200 Production, Sup...

NVIDIA’s Blackwell generation extends beyond chip-level upgrades to full-system design, deployment models, pricing, and margin strategy. This analysis outlines the key product variants, packaging and memory choices, expected ramps, indicative...

Ramp Outlook: B100, B200, GB200 Production, Sup...

NVIDIA’s Blackwell generation extends beyond chip-level upgrades to full-system design, deployment models, pricing, and margin strategy. This analysis outlines the key product variants, packaging and memory choices, expected ramps, indicative...